Our view of global markets

The “Trump effect”- Donald Trump’s return to the White House is set to be a game-changer for the US economy and markets. We think the likelihood of more fiscal stimulus and deregulation may drive growth and provide a tail wind fo risk assets, at least in the short term.

- We still consider a “soft landing” as the most likely outcome for the US economy, where inflation slows and recession is avoided. But we see an increasing risk of a “no landing” where growth reaccelerates and inflation takes off again. This would likely have implications for US monetary policy.

- Globally, the second Trump term comes as economies diverge in growth, inflation and interest rates. We see this divergence widening in 2025.

- Fresh thinking and broader diversification are advisable. Diversification might include private market assets, particularly if rising inflation reverses the recent decorrelation between stocks and bonds.

- Given the Trump effect, we are positive on US equities but are conscious of high valuations. In fixed income, we like Europe over the US, as anticipated European rate cuts are more likely to remain intact. The sequencing of the policies of the incoming US administration will be key in determining the trajectory of financial markets in 2025.

- From tariffs to political paralysis in the euro zone, geopolitical risk will loom large but unevenly across markets, requiring a deft approach to managing a portfolio.

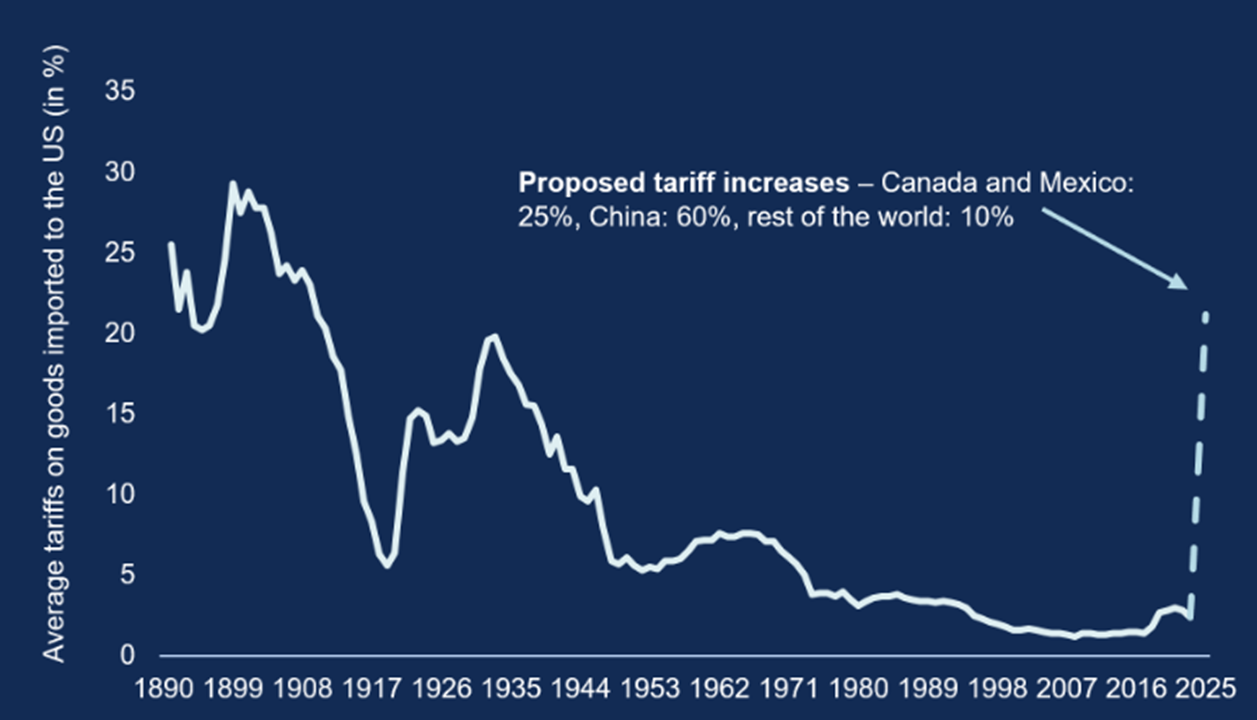

Source: Allianz Global Investors Global Economics & Strategy, Bloomberg, United States International Trade Commission (data as at 27 November 2024). Note: chart assumes tariff rates will rise from current levels to those indicated by Mr Trump.

Source: Allianz Global Investors Global Economics & Strategy, Bloomberg, United States International Trade Commission (data as at 27 November 2024). Note: chart assumes tariff rates will rise from current levels to those indicated by Mr Trump.Asset class convictions

Equities- Overall, we remain constructive but expect a pick-up in volatility as more detail emerges of how new US policy – particularly on immigration and tariffs – might impact inflation and global supply chains. So, we continue to favour volatility-absorbing strategies in the multi-factor space to anchor portfolios.

- We still like the US and remain keen on technology stocks at the right valuation given their innovation and earnings profile. A broadening in technology sector performance is likely in 2025.

- European valuations are favourable, and interest rate cuts could be more pronounced than in the US, supporting selective exposure to companies with global earnings resilience.

- India’s young population is fuelling an “aspiration economy” and its relatively neutral position versus both the US and China may give its exporters an edge in a more protectionist world.

- Despite negative market sentiment, we continue to favour some China exposure in global portfolios. Support for its domestic economy – and recent reform of its private pension programme – could boost the market beyond current expectations.

- We favour European bond markets relative to the US. While weaker growth in Europe will likely keep rate cuts intact, the Fed could scale back rate cuts in the US in H1 as the Trump agenda drives domestic growth. We maintain a curve steepening bias in both markets but have tactically taken some profits (or reduced our exposure).

- Think about active portfolio construction in fixed income. Outright duration calls should be balanced with relative value trades across regions, currencies and curve positioning – amid greater divergence across economies.

- We think UK gilts are a good place to be as the market is underpricing the scope for rate cuts.

- In corporate credit, we think valuations of investment grade bonds are more attractive in Europe than in the US (and prefer IG over high yield). But in an unpredictable environment, this asset class calls for active management and diversification.

- With uncertainty and potential currency volatility ahead, we think investors should position themselves in the middle to lower end of risk budgets, so they have room to react.

- While the S&P 500 remains our favoured equity market, we have softened our stance amid question marks over the longer-term outlook – we want to be prepared for setbacks. US small caps should thrive in a Trump economy.

- Japan is a favoured equity market outside the US as it could be less vulnerable to tariff attacks than many other Asian countries, while also benefiting from falling energy prices and solid earnings revisions.

- We await any impact that new US policy has on the dollar. While we remain constructive on the greenback for the moment, any dollar weakening might be a chance to reallocate funds to asset classes that came under pressure around the time of the US election such as EM debt. We are increasingly positive on the yen.

- Gold is back as a useful diversifier in multi-asset portfolios. Since the US elections, the downward pressure on the gold price exerted by a strong US dollar and high real interest rates has been counterbalanced by demand from central banks and from retail investors in China and India.

- We think now is a good time for assets uncorrelated with the rest of the market – such as carbon credits or volatility as an asset class in its own right – that can generate value while actively managing risk in portfolios.

Importance NoticeThis document is for general information only. The information or opinion herein is not to be construed as professional investment advice or any offer, solicitation, recommendation, comment or any guarantee to the purchase or sale of any investment products or services. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. The investment products or services mentioned in this webpage are not equivalent to, nor should it be treated as a substitute for, time deposit, and are not protected by the Deposit Protection Scheme in Hong Kong.The information or opinion presented has been developed internally and/or taken from sources (including but not limited to information providers and fund houses) believed to be reliable by WeLab Bank, but WeLab Bank makes no warranties or representation as to the accuracy, correctness, reliabilities or otherwise with respect to such information or opinion, and assume no responsibility for any omissions or errors in the content of this document. WeLab Bank does not take responsibility for nor does WeLab Bank endorse such information or opinion.Investment involves risks. The price of an investment fund unit may go up as well as down and the investment funds may become valueless. Past performance is not indicative of future results. WeLab Bank makes no representation or warranty regarding future performance. Any forecast contained herein as to likely future movements in interest rates, foreign exchange rates or market prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in interest rates, foreign exchange rates or market prices or actual future events or occurrences (as the case may be).You should not make any investment decision purely based on this document. Before making any investment decisions, you should consider your own financial situation, investment objectives and experiences, risk acceptance and ability to understand the nature and risks of the relevant product(s). WeLab Bank accepts no liability for any direct, special, indirect, consequential, incidental damages or other loss or damages of any kind arising from any use of or reliance on the information or opinion herein. You should seek advice from independent financial adviser if needed.WeLab Bank is an authorised institution under Part IV of the Banking Ordinance and a registered institution under the Securities and Futures Ordinance (CE Number: BOJ558) to conduct Type 1 (dealing in securities) and Type 4 (advising on securities) regulated activities.This document is issued by WeLab Bank. The contents of this document have not been reviewed by the Securities and Futures Commission in Hong Kong.