Invesco’s 2025 Investment Outlook – Asia Equities

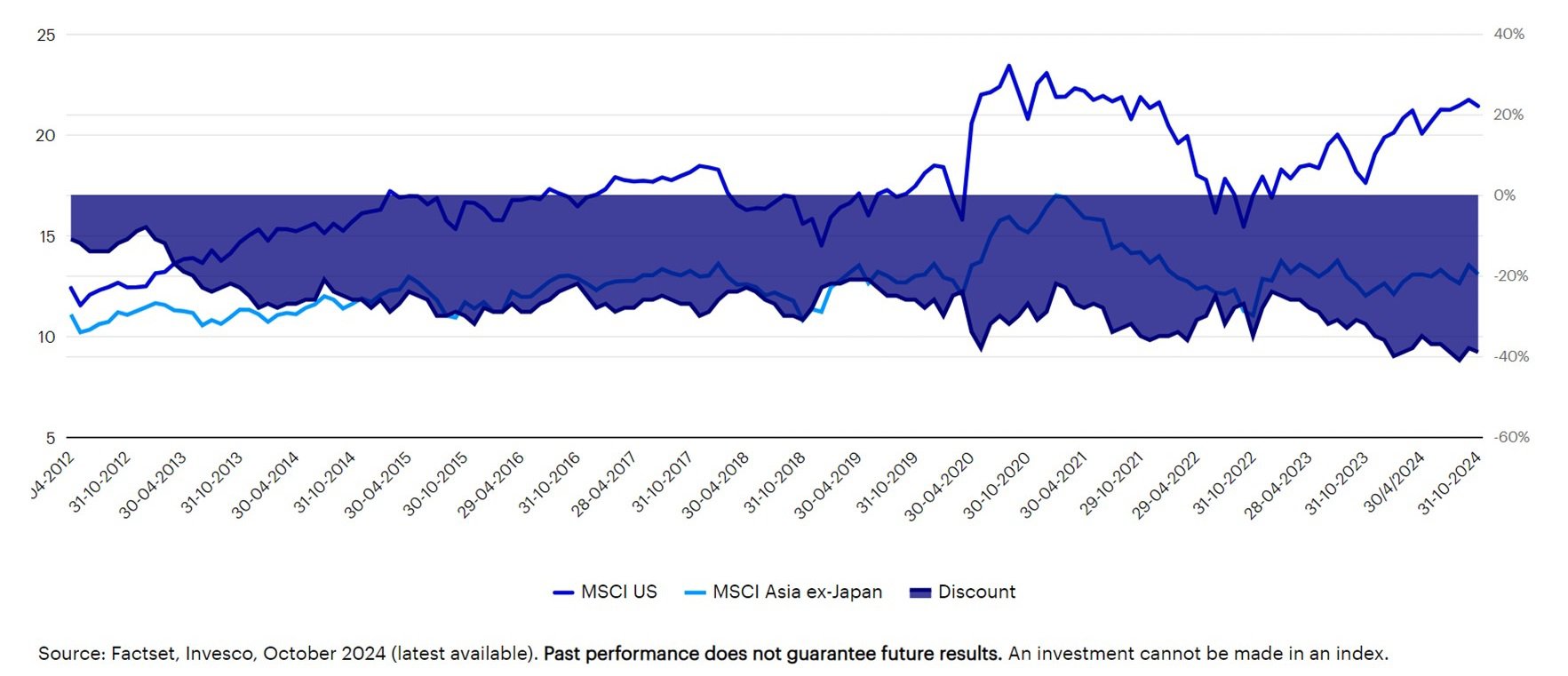

Asia’s macroeconomic backdrop improved in 2024 and equity market performance in the region remained strong. Elections occurred in several major Asian countries during the early part of the year which have largely helped to create a stable economic environment. The US Federal Reserve also recently started their easing cycle as inflation is coming under control. Looking ahead to 2025, we expect domestic demand in the region to strengthen as the effects of earlier monetary tightening wane. We also think increased intra-regional trade driven by China's economic recovery will enhance exports and consumption. We are focused on domestic drivers of the Asian market as an indicator of the region’s economic trends.Increasing certainty in Asia's path toward monetary easingAsia has successfully reduced inflation and kept interest rates at a stable level more quickly than the rest of the world. The Philippines, Indonesia, Thailand, and Korea began their rate cutting cycles in Q3 2024. With the Federal Reserve now having started its easing cycle, Asian countries will have more room to lower interest rates in 2025, alleviating concerns about potential currency pressures.Stimulus package fuels China's economic recoveryThe Chinese government recently announced a raft of stimulus measures aimed at stabilizing the stock market and property market. We believe these policies will help to create opportunities for future economic growth. Looking ahead, we have a positive outlook for China. We expect policy support to continue with more measures being implemented in the near term. We have already observed a positive impact from the September stimulus efforts including an uptick in manufacturing activity. We also expect China's recovery to create opportunities for other Asian economies by enhancing intra-regional exports notably to ASEAN markets. We expect commodities and service exports, such as tourism and transportation, to benefit from this recovery.Domestic demand as a catalyst for structural growth in Asia🔹 IndiaIndia is projected to be the strongest growing major emerging market economy this year, fueled by rising consumer sentiment and increased spending. Retail sales have surged, particularly in discretionary categories, thanks to a large young population with rising disposable income. We believe the continuation of labor market reforms, increasing push for infrastructure development, and enhancements in education and workforce skills, all present significant opportunities for higher economic growth in 2025 and beyond.🔹 ASEANOur economic outlook for the ASEAN region remains robust and we are positive on Singapore, Malaysia, Indonesia, and the Philippines. The structural growth of ASEAN markets, characterized by young demographics and rising incomes, supports strong domestic consumption and investment. Foreign direct investment (FDI) inflows have surged from US $170 billion in 2016 to $220 billion in 2023.1 Looking ahead, we think the recovery of global trade and tourism will be a key growth driver. We believe countries like Singapore and Malaysia are well-positioned to benefit from increased FDI and export growth. International tourism within ASEAN is steadily recovering, nearing pre-COVID levels, and we expect this positive trend to continue.Structural dynamics of the AI tech cycle🔹 Taiwan and KoreaTaiwan and Korea are global leaders in semiconductor manufacturing. The rising demand for artificial intelligence (AI) technologies is expected to drive investments in advanced chip production and research and development, bolstering economic growth. We anticipate that the AI sector will continue to fuel strong earnings growth for these two markets. In Taiwan, earnings revisions are expected to remain positively biased due to strong structural growth in AI and a potential cyclical recovery in non-AI tech demand in 2025. In Korea, the tech-driven export recovery is maturing, and the domestic economic outlook is likely to improve given the start of the monetary easing cycle. We also expect the structural uptrend in AI to benefit Korea’s IT supply chain.🔹 Potential headwindsLooking ahead we will monitor several key factors that may impact the performance of Asian economies in 2025. First, we will keep an eye on retail and loan growth in the region. Second, we will scrutinize the policies being implemented by the Trump administration for their potential impact on Asian countries, particularly export-driven economies. Third, we will examine global demand as a reduction in demand could affect investor confidence in the region. Asian governments are actively implementing policies to foster growth and maintain stability. We believe the extent of China’s recovery will significantly benefit Asian markets. As China’s economic momentum accelerates, we expect the increase in demand for goods and services will stimulate growth in neighboring countries and lead to upward revisions in corporate earnings across the region.🔹 Risk-reward profile of Asian equities looks attractiveFrom a valuation perspective, Asian markets appear attractive, with Asia ex-Japan equities currently trading at a low forward 12-month price-to-earnings ratio of 13.1x, which is less than one standard deviation below the long-term average.2 In comparison to developed markets, Asia ex-Japan equities are trading at approximately a 39% discount.3 We are optimistic about the earnings growth potential of Asian corporations, with market consensus projecting double digit earnings per share growth in the coming year.4 This positive outlook suggests further upside for earnings and return on equity, driven by an improving economic environment in Asia.Figure 1 – Asia ex-Japan equities still trading at a discount to developed markets Investment risksThe value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested.When investing in less developed countries, you should be prepared to accept significantly large fluctuations in value.Investment in certain securities listed in China can involve significant regulatory constraints that may affect liquidity and/or investment performance.

Investment risksThe value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested.When investing in less developed countries, you should be prepared to accept significantly large fluctuations in value.Investment in certain securities listed in China can involve significant regulatory constraints that may affect liquidity and/or investment performance.

Footnotes1 Southeast Asia: Foreign investments resilient despite global economic uncertainties, October 2024.2 Source: Factset, data as of October 2024.3 Ibid.4 Goldman Sachs, data as of 2 November 2024.Want to search and invest in related funds?Open the WeLab Bank App and click【Featured Funds】to find out more!

Importance NoticeThis document is for general information only. The information or opinion herein is not to be construed as professional investment advice or any offer, solicitation, recommendation, comment or any guarantee to the purchase or sale of any investment products or services. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. The investment products or services mentioned in this webpage are not equivalent to, nor should it be treated as a substitute for, time deposit, and are not protected by the Deposit Protection Scheme in Hong Kong.The information or opinion presented has been developed internally and/or taken from sources (including but not limited to information providers and fund houses) believed to be reliable by WeLab Bank, but WeLab Bank makes no warranties or representation as to the accuracy, correctness, reliabilities or otherwise with respect to such information or opinion, and assume no responsibility for any omissions or errors in the content of this document. WeLab Bank does not take responsibility for nor does WeLab Bank endorse such information or opinion.Investment involves risks. The price of an investment fund unit may go up as well as down and the investment funds may become valueless. Past performance is not indicative of future results. WeLab Bank makes no representation or warranty regarding future performance. Any forecast contained herein as to likely future movements in interest rates, foreign exchange rates or market prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in interest rates, foreign exchange rates or market prices or actual future events or occurrences (as the case may be).You should not make any investment decision purely based on this document. Before making any investment decisions, you should consider your own financial situation, investment objectives and experiences, risk acceptance and ability to understand the nature and risks of the relevant product(s). WeLab Bank accepts no liability for any direct, special, indirect, consequential, incidental damages or other loss or damages of any kind arising from any use of or reliance on the information or opinion herein. You should seek advice from independent financial adviser if needed.WeLab Bank is an authorised institution under Part IV of the Banking Ordinance and a registered institution under the Securities and Futures Ordinance (CE Number: BOJ558) to conduct Type 1 (dealing in securities) and Type 4 (advising on securities) regulated activities.This document is issued by WeLab Bank. The contents of this document have not been reviewed by the Securities and Futures Commission in Hong Kong.